A rate “normalization” that still hasn’t reached what was “normal” in 2007,

and “quantitative tightening” that has yet to make a significant dent in the balance sheet.

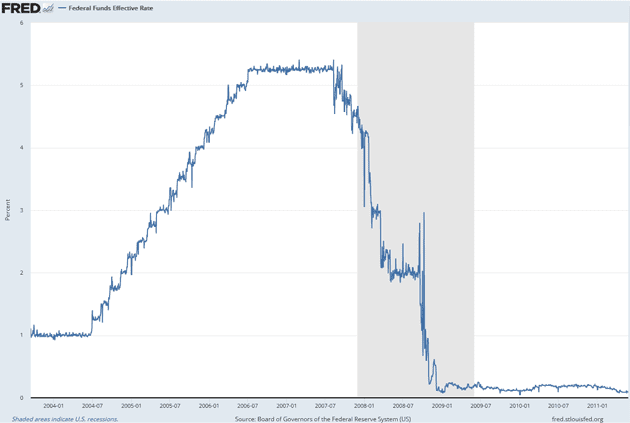

By summer of 2004 the Fed thought it was time to raise rates, and it did so steadily for the next two years. Whether that tempered growth is still unclear. It may be that the prospect of higher rates made people even more eager to buy homes (and lenders more eager to finance them) before rates rose further.

Regardless, in late 2007 it was pretty clear something was amiss. Deals were blowing up, fund managers running into trouble, etc. Not seriously so, but enough to warrant a response. So began the rate cuts.

Then in 2008 Bear Stearns imploded, followed months later by Lehman Brothers.

Late 2008 fed funds was approaching zero and people were asking, quite reasonably, what the Fed would do next. At the time, the “QE” (quantitative easing) that is now so familiar to us was just an obscure academic concept.

It became more than academic in November 2008 when the Fed announced it would purchase $600 billion in agency mortgage-backed securities (Fannie Mae, etc.) and associated debt. This, combined with the zero-bound fed funds rate reached the following month, was to be the solution.

Six more years of zero rates and vast asset purchases, a half-hearted attempt to normalize before Jerome Powell “crawdadded,” (walked backwards) as I called his seeming surrender to markets at the time.

Then two more years of ZIRP after COVID struck and now a rate “normalization” that still hasn’t reached what was “normal” in 2007, and “quantitative tightening” that has yet to make a significant dent in the balance sheet.

Until last year, many knew nothing but zero or very low rates and a stock market with highly favorable tailwinds. Even some graybeards let hope get the best of them, thinking it really was different this time.

But the years of easy money didn’t just boost markets. They changed the economy itself.

Rather than reinvest profits to grow the business, low interest rates make it more attractive to buy their competitors, or use borrowed cash to buy back their own shares.

Not so long ago one could accumulate a nest egg, invest it in simple, low-risk bonds and generate good income. That became impossible under ZIRP and still is today since inflation has overwhelmed the benefit of higher yields.

I am perfectly comfortable with 5% interest rates when inflation is 4‒5%. I hope rates stay high enough to give investors a real return on their savings, and less incentive to buy your competition rather than actually invest and compete.

John Mauldin 3 March 2023

https://www.mauldineconomics.com/frontlinethoughts/how-it-started-how-its-going

Kommentarer